NVDA is remarkable. It's also too big.

Why their bull case and bear case both point elsewhere.

I was long NVDA again for 3 hours yesterday. The company is of the highest caliber, has not participated as much as they deserve in the fantastic rally in semis this season, and seemed ripe for some recognition. The thesis was to capture any information reveal then move back to more convex opportunities.

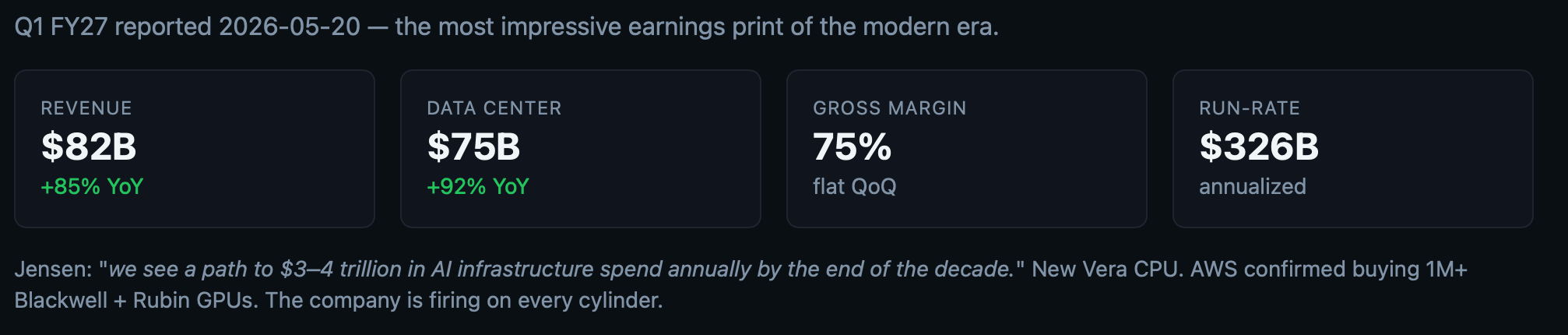

Numbers out, crushed without a blemish, reaction muted. Moving on.

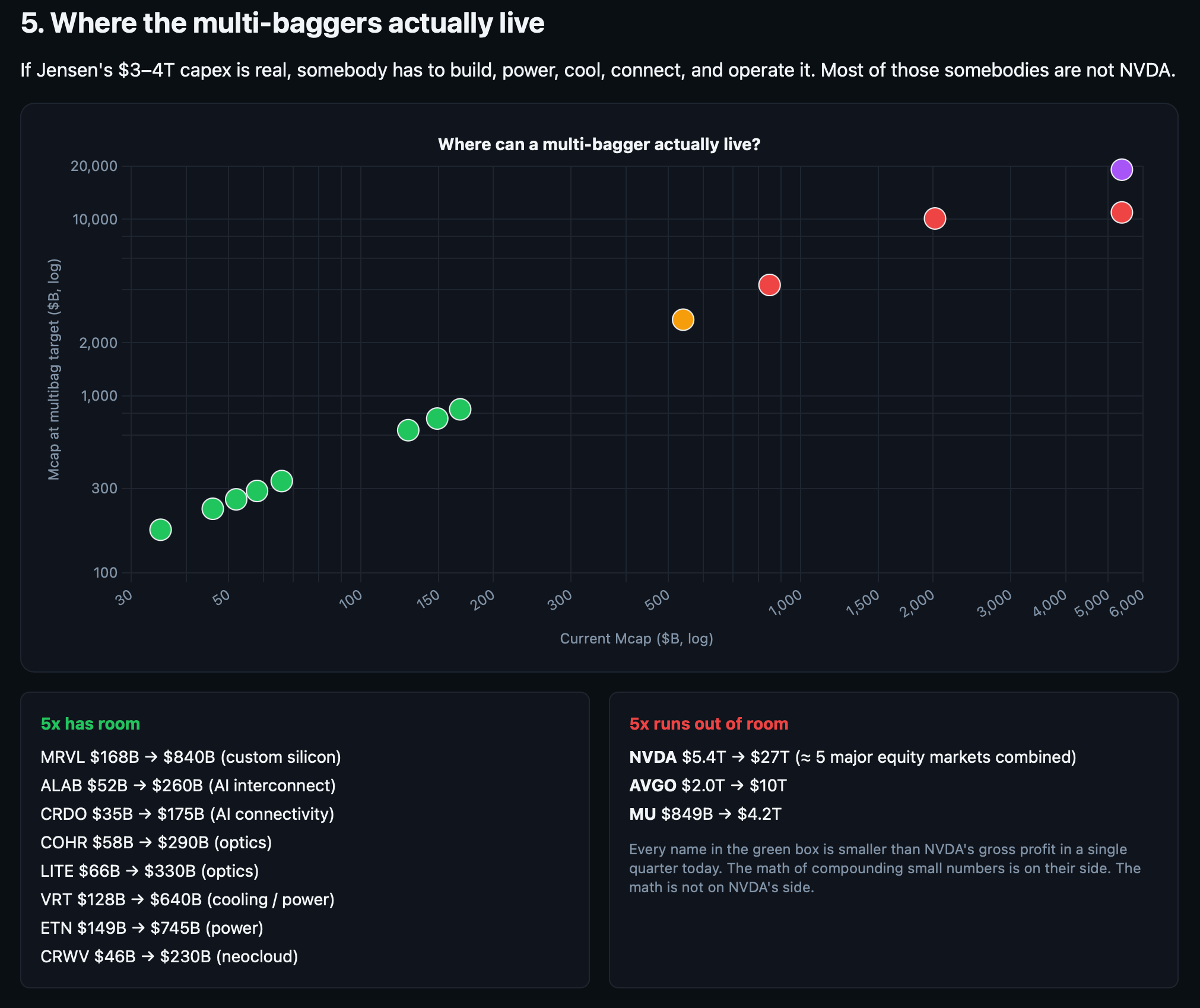

Market cap is one of my favorite vibe metrics for eyeballing an opportunity. In fact, my biggest successes this year (AMD, Intel) were due entirely to this phenomena. If you project the happy path forward where NVIDIA is a 10 trillion company, does it make sense that Intel (the only credible advanced domestic foundry) and AMD would hold a market cap of 100b and 250b respectively? No. One way or the other they would chip off more than 3% on a relative basis.

Don’t settle

If I can’t tell a simple story as to why a play has a chance of being high-skew over the next 2 years in addition to clear momentum and thematic fit, then I’ve given up before even starting.

Marvell and Nokia seem to be two candidates that have the right headroom, added both. Going to circle back on that later but found good primers out there from Gaetano if you’re curious why.

—

Full microsite here: https://macrodesk.ai/share/nvda-too-big/dacbba12/c

—