Semis: Be careful betting on Single Names vs. ETFs.

Don’t overpay for “dispersion premia” that you aren’t using. Or why I moved my semis deltas to 71% SOXX 29% single name vs. 100% single name.

In my quest to get As Long As Possible™, there’s an important thing that needs to be managed. When using call options / LEAPs for convexity, there’s a cost to placing bets on individual companies vs. the sector when your view is evenly bullish. This isn’t news to professional options traders but for those just trying to get the exposure they crave, read on.

Allow me to give a concrete example.

AVGO is really interesting, Mythos was trained entirely without NVIDIA in the stack. Let’s lever up with some 50 or 35 delta LEAPs.

Intel is a no brainer, it’s the only credible path to domestic advanced foundry. Add LEAPs.

NVDA is cheap right now, it’s being punished for its size and stickiness to the S&P, in the short to medium term it certainly has room to run. More options.

Memory isn’t cyclical, it’s a new secular trend trading at 8x fwd P/E. Let’s ride the momentum and pick up some shorter tenor debit spreads.

AMD is a catch up trade, whatever it’s worth, if NVDA is going to 6 trillion then AMD must go to 1 trillion, 100% upside.

.. and so on.

Next thing you know you’re holding 15 names… if these were normal equity positions that would be no problem, and perhaps desirable for tax loss harvesting. However, if you are using options to lever up your theme beta, you could be overpaying dramatically.

2. What’s the issue?

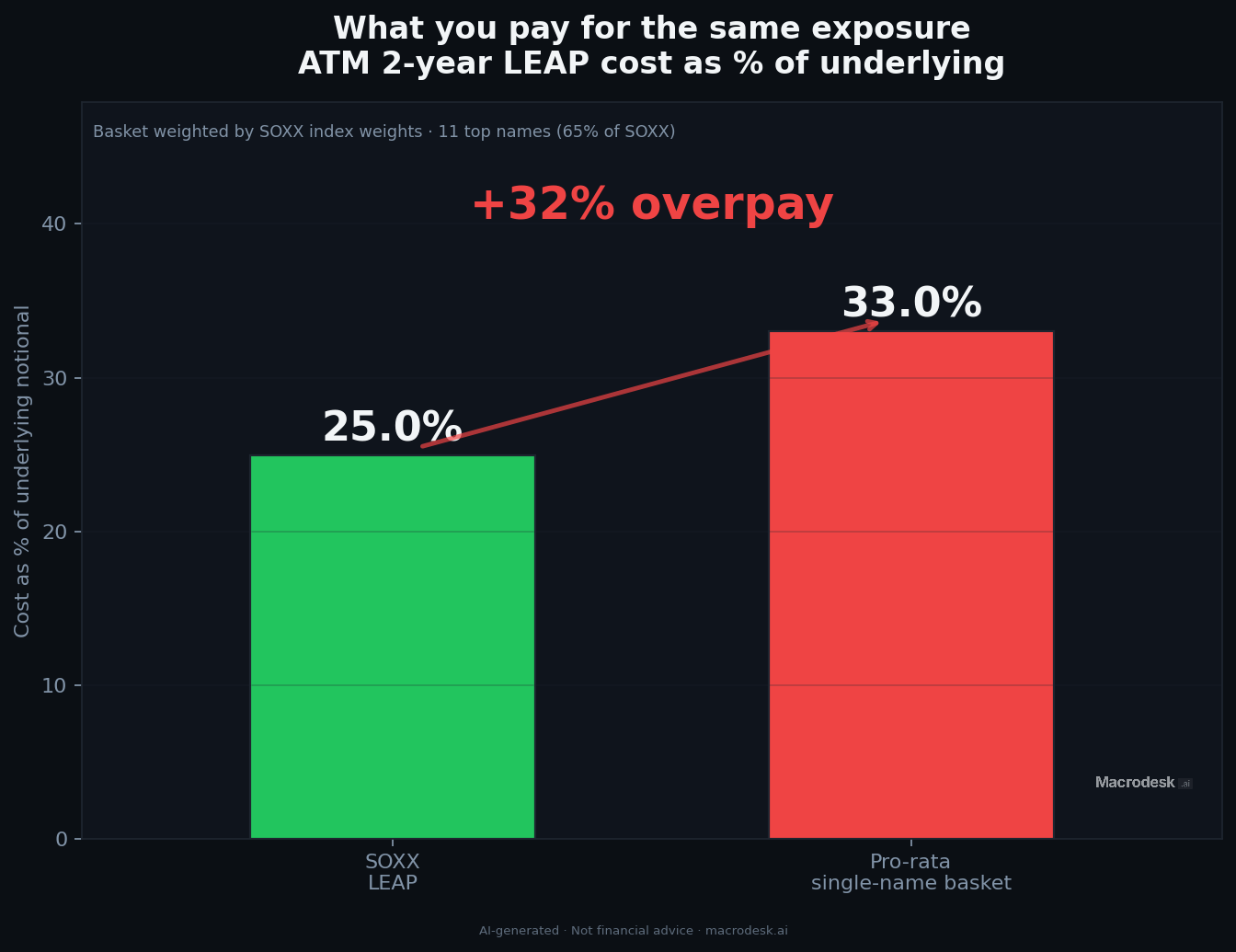

When you place a bet in this way, you’re making a directional bet but also betting that the magnitude of the move over that period is larger than what the market expects and has priced. Take SOXX as an example, which has a generally even 5-10% allocation to the above ideas.

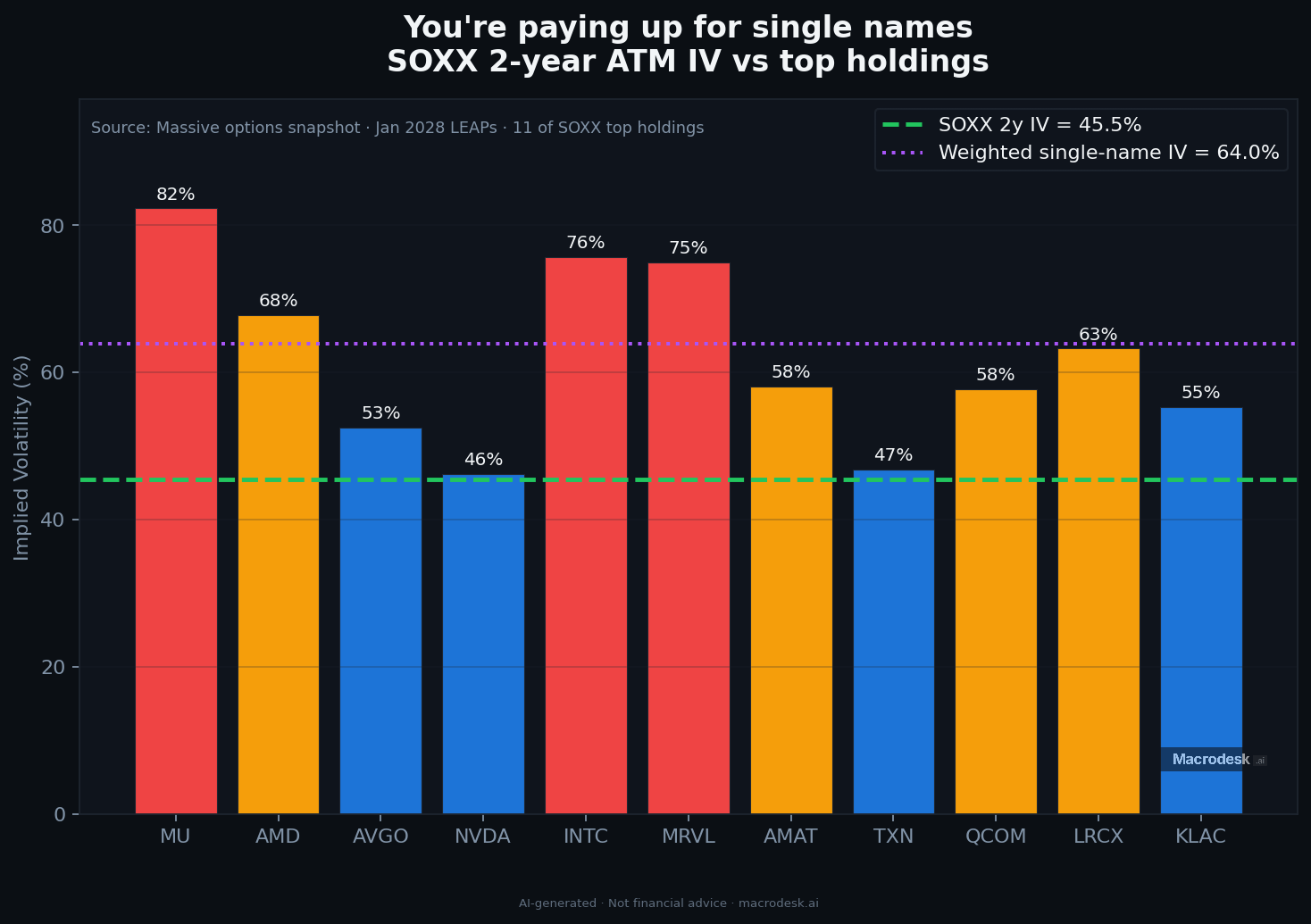

SOXX may have a 43% IV for LEAPs 2 years out

Micron on the other hand may have an IV of 80%+ over the same period, same for Intel AMD etc.

If you were to bet on every name in this way on a pro-rata basis, you may be paying an average IV of 64% vs. 45% for the ETF itself. People pay a huge premium for the privilege of betting on single name outperformance.

3. Why does this happen?

Because individual moves partially “cancel out” inside of the ETF, the ETF itself is less volatile and carries lower premiums. There are professional “dispersion traders” that specialize on isolating this and trading it directly but we just need to be aware of it.

4. How I approach this

When I am bullish on a dozen names in the ETF for distinct reasons, this is actually the ideal time to bet on the ETF itself. Because the IV implies winners and losers when I see mostly winners (i.e. correlated), there’s a discount to harvest. For the single name bets, I limit these to the 2 or 3 that I feel will not only beat but CRUSH their individual IVs. Generally this means multibag potential for something like a Micron or Intel. I had that conviction on Intel when it was trading below a 100b market cap, but now I’m more uniformly bullish on it vis-a-vis the rest of the names in SOXX after a 450% rally.

5. The key point

You need to be VERY bullish on your single names when you’re paying up for high-IV names. Otherwise you may be better off betting on the sector itself. Don’t open more than a few positions until you understand this.

6. Bonus: what’s worth the premium to me today?

I like Marvell due to it being a mixture of the Intel and AVGO thesis - has the market cap shape to multibag and is in place for the explosion of alternative ASICs. Worth the extra premia.

I also like AVGO for the opposite reason, IV is actually looking very attractive (comparable to SOXX itself) but with a higher level of conviction vs. the sector itself.

I feel the same about Oracle but that’s a story for another day. Perhaps Capital Flows could chime in on this one.

What companies are you willing to pay 100% IV for?