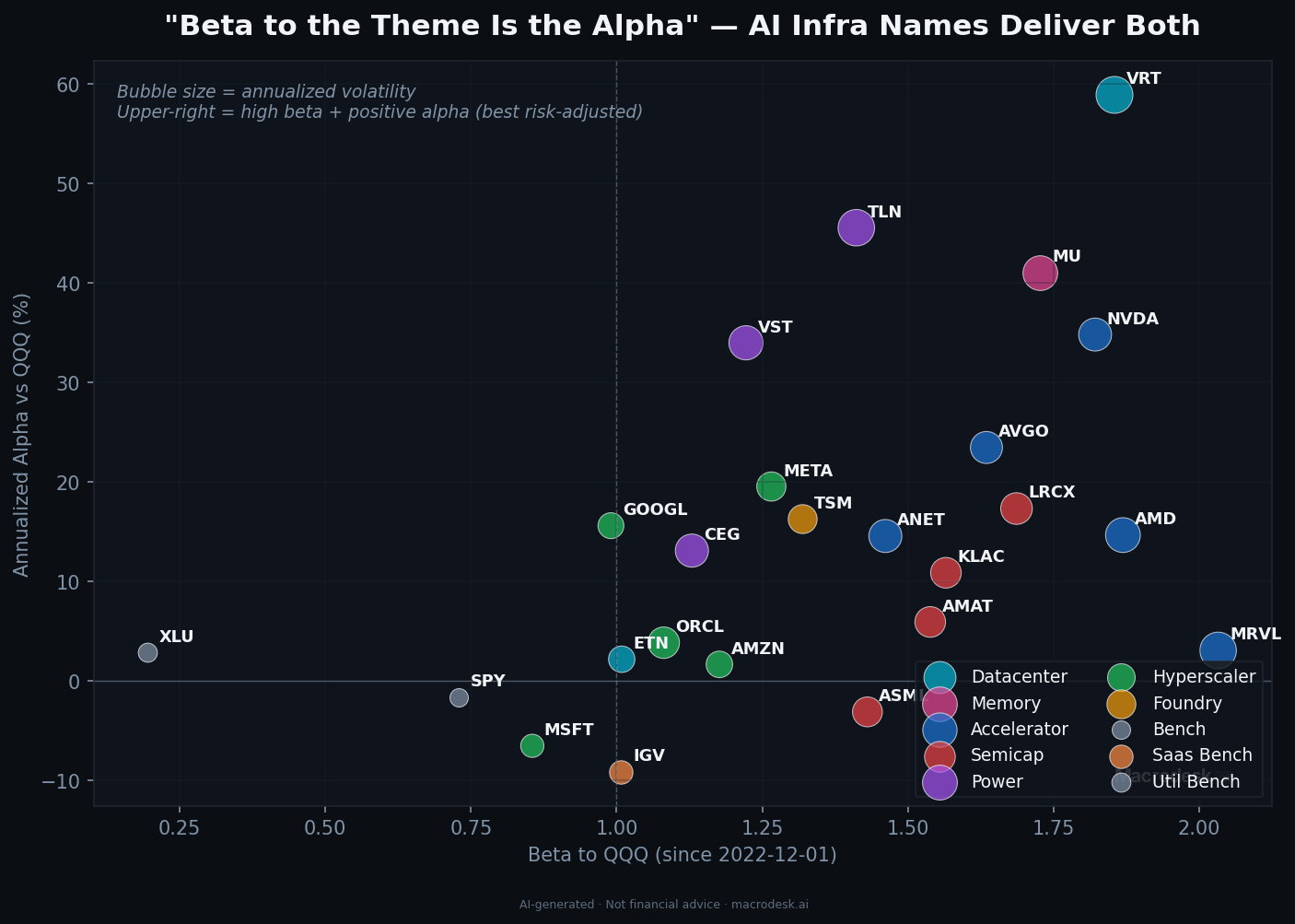

Theme-beta is the Alpha: AI Capex is Inelastic.

Beyond chasing charts: do the Mythos trendlines and OpenAI's Erdős breakthrough make tapping the Capex brakes extremely improbable?

Whenever volatility is cheap, I do add to my tail hedges to avoid a wipeout in a major shock. Usually 10% OTM puts on the SPX up to about 100-200bps of premium. However, if the promise of these models does not materialize and the whole thing rolls over, then poof. This is the risk / reward of levered exposure to takeoff.

Sustaining this exposure can sometimes feel like momentum chasing or meme stock mania. I have to replenish my conviction from time to time to remember what the Alpha is, which is front-running the mid to long term reaction to what is unfolding.

What we already know:

A few current events

Google just reaffirmed their expanded Capex plans, cloud backlog (2x due to Anthropic later widely cited) and indicated an unspecified INCREASE for next year: Q1 2026 GOOGL call (April 29, 2026)

Anat Ashkenazi, CFO: “We are updating our full year 2026 CapEx guidance range to $180 billion to $190 billion, up from our previous estimate of $175 billion to $185 billion to now include investment related to the acquisition of Intersect…”

“We expect our 2027 CapEx to significantly increase compared to 2026.”

NVIDA re-confirmed the same, forecasting 3T in total annual Capex by 2030 (not just hyperscalers), FY27 Q1 (May 20, 2026):

“With analysts now forecasting hyperscale CapEx to exceed $1 trillion by 2027 and Agentic AI beginning to proliferate all industries, AI infrastructure spending is on track to reach $3 trillion to $4 trillion annually by the end of this decade.”

For the risk tolerant, these breadcrumbs justify ratcheting up the bets on AI infrastructure, semis, and hyperscalers over the next few years.

But is it inelastic?

Perhaps we should take the time to look at what’s happening that may preclude any of these major players from pulling back in the foreseeable future regardless of the macro regime.

1. Claude Mythos

Beyond the cyber-security aspects and Project Glasswing, look at the benchmarks:

That’s a gigantic gap up - regardless of nuance around cost to serve. Not just holding, but a discontinuity. Google, who appeared to be in the drivers seat with Gemini 3, now feels 6 months behind. The race is on.

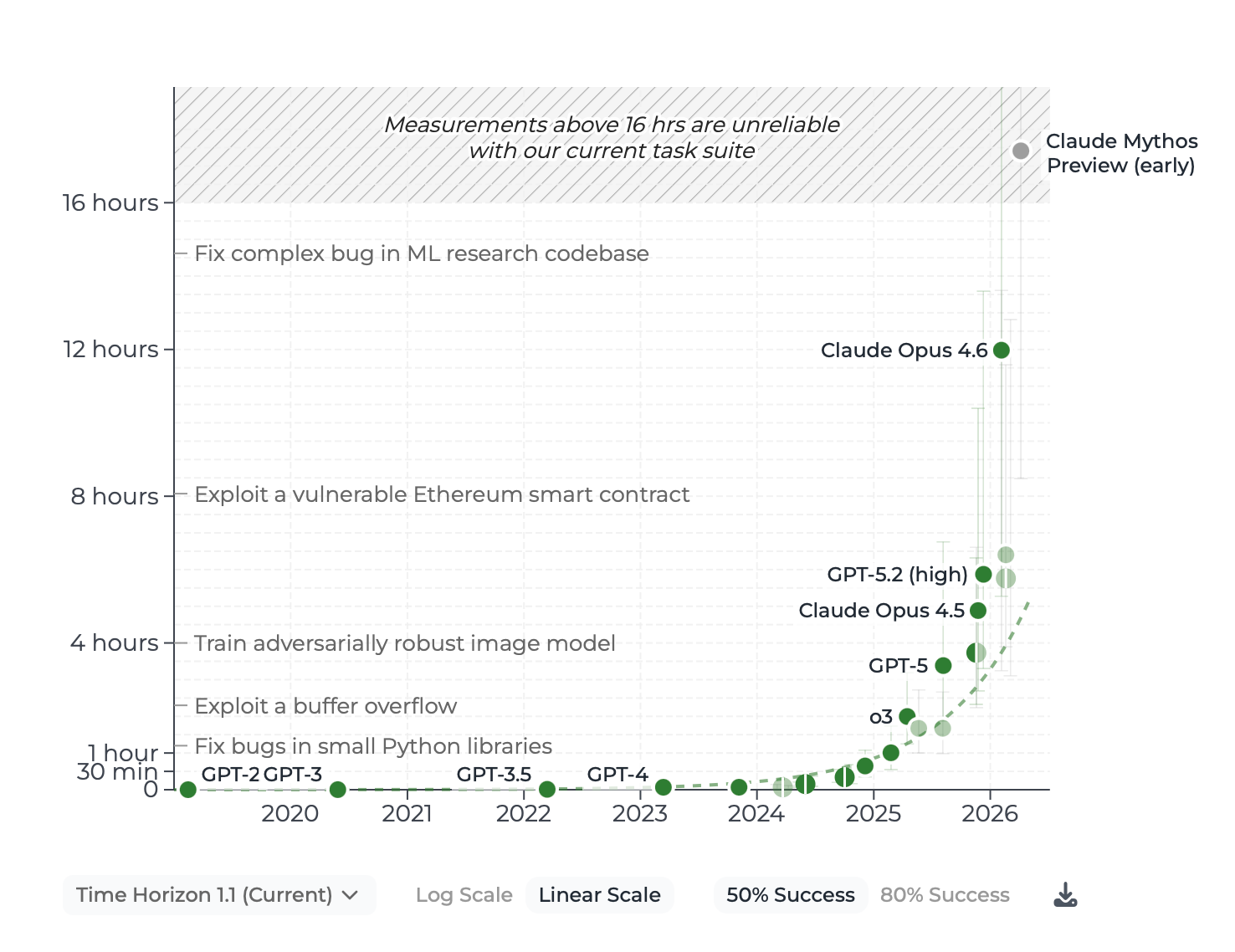

Look at this chart from METR (if you aren’t familiar with METR trendlines, brush up):

Does this look like a good time to cancel planned capacity you can afford in any case and with cloud revenues growing 63% YoY?

2. An OpenAI model has disproved a central conjecture in discrete geometry

We had IMO gold, now this.

One of the confirmation signals I have been personally waiting for is a unique contribution that isn’t long tail:

an autonomous company turning a profit

novel drug discovery

cracking of a major unsolved proof like a millennium problem

Materials science, even if shy of a room temperature superconductor

TLDR; Paul Erdős was a prolific mathematician that posed over a thousand problems (half unsolved) that have attracted various levels of professional human effort. With (disputed) buzz around models tackling some of these, OpenAI disproved a major one.

While this feels halfway there, there’s an asymmetry for me. It seems to tip the scale from “possible” to “nearly guaranteed” re: the revelation of a major discovery or solution within the next few years. These headlines will likely continue and their implications will sink in.

UPDATE: Google DeepMind just announced they have paired LLMs with the Lean language to solve 9 more, including 2 that have been unsolved for 56 years. Not an expert, but the headlines are trickling in.

What does this have to do with capex being inelastic?

The decision makers in this race see these trendlines and capability discontinuities and can’t afford to be caught out. It’s existential. This isn’t a new argument, but it’s probably essential to the idea to doubling down over and over on a cyclical sector.

A counterargument in the mid-term

What about the marginal AI infrastructure Capex customer? It’s pretty clear that the risk/reward for all of the major players will result in full steam ahead regardless of the macro picture, but what about the marginal buyers if a bond scare or headline scare like the Saaspocalypse triggers some reflexivity? In the mid term, I think it is worth defining who those marginal customers are and watching closely. Stay tuned.